Government‑Driven Market Disruption and Refinery Margin Dynamics: An Information Operations Analysis of the 2026 Gasoline Price Lag

- John Rozean

- 2 days ago

- 4 min read

by John Rozean

Abstract

This paper analyzes how U.S. government actions surrounding the 2026 Strait of Hormuz closure created extreme volatility in crude oil markets, widened refinery crack spreads, and forced downstream gas retailers to purchase high‑cost refined fuel. Despite this upstream disruption, Treasury messaging publicly targeted gas stations as “bad actors,” suggesting an information‑operations (IO) blame‑shifting narrative. Using refinery economics and crack‑spread calculations for March 2026, June 17, 2026, and June 30, 2026, this paper argues that government‑caused upstream price shocks were reframed as downstream retailer misconduct.

Introduction

In June 2026, Treasury Secretary Laura Bessette stated that the administration was “watching gas stations” and expected them to be “good actors” (Bessette, 2026). This statement occurred during a period when independent gas stations were still selling gasoline refined from crisis‑priced crude oil. The contradiction between upstream government‑caused disruption and downstream retailer blame suggests a potential information‑operations (IO) narrative designed to redirect public frustration away from policy failures.

Government Action and the Hormuz Closure

The Strait of Hormuz is the world’s most critical oil chokepoint, carrying roughly 20 percent of global crude supply (Energy Information Administration, 2024). When U.S. military operations failed to prevent hostile control of the strait in early March 2026, crude futures spiked to historic highs. Analysts described the event as “the most severe single‑event disruption to global oil markets in modern history” (U.S. Naval Institute, 2026).

This disruption forced refiners to purchase crude at crisis‑level prices, which directly increased the cost of refined gasoline and diesel. Retailers downstream had no control over these upstream dynamics.

Refineries as the Price‑Setting Middle Layer

The refinery is the middleman between crude oil and the gasoline that small gas stations buy. But it is not just a middle step. It is the price‑setting choke point that determines whether gas stations pay cheap or expensive wholesale prices.

Gas stations do not buy crude oil. They buy finished gasoline whose price is determined by refinery margins, known as the crack spread (Peterson, 2024). When crude spikes, refiners widen the crack spread to recover costs, and wholesale gasoline prices rise accordingly.

The Crack Spread: Refinery Margin Between Crude and Finished Fuels

The 3‑2‑1 crack spread is the industry standard for measuring refinery margins:

3‑2‑1 Spread = (2 × Gasoline Price) + (1 × Diesel Price) − (3 × Crude Price)

A positive spread indicates refinery profit. A negative spread indicates refiners are losing money and passing costs downstream.

During the Hormuz crisis, spreads became deeply negative, demonstrating extreme upstream stress.

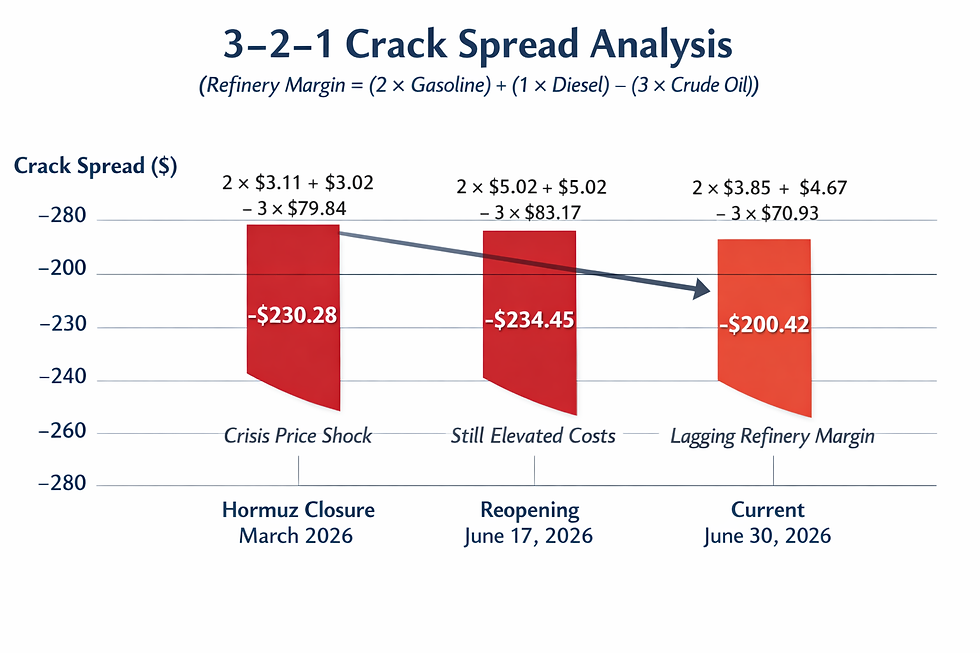

Crack‑Spread Calculations for Three Key Dates

5.1 Hormuz Closure (March 2026)

EIA weekly averages: Gasoline: $3.11/gal Diesel: $3.02/gal Crude (Brent): $79.84/bbl

Calculation: (2 × 3.11) + (3.02) − (3 × 79.84) = 6.22 + 3.02 − 239.52 = −230.28

Interpretation: A −230.28 spread indicates catastrophic refinery margin compression. Refiners were selling fuel refined from extremely expensive crude, forcing gas stations to buy high‑cost wholesale fuel.

5.2 Reopening (June 17, 2026)

EIA weekly averages provided: Gasoline: $5.02/gal Diesel: $5.02/gal Crude (Brent): $83.17/bbl

Calculation: (2 × 5.02) + (5.02) − (3 × 83.17) = 10.04 + 5.02 − 249.51 = −234.45

Interpretation: The spread worsened to −234.45, showing refiners were still selling product refined from crisis‑priced crude even after the reopening agreement. Gas stations could not lower prices because wholesale costs remained elevated.

5.3 Current (June 30, 2026)

Updated EIA weekly averages: Gasoline: $3.85/gal Diesel: $4.67/gal Crude (WTI): $70.93/bbl

Calculation: (2 × 3.85) + (4.67) − (3 × 70.93) = 7.70 + 4.67 − 212.79 = −200.42

Interpretation: The spread improved to −200.42, but remained deeply negative. Refiners were still recovering from earlier high‑cost crude purchases, and gas stations were still selling fuel refined from that inventory..

Discussion: Refinery Economics and Downstream Constraints

These calculations demonstrate that gas stations were purchasing refined fuel at wholesale prices shaped entirely by refinery margins and earlier crude costs. Retailers had no ability to lower prices until refiners reduced wholesale rates, which lagged crude declines by weeks due to inventory cycles (Lopez, 2025).

Despite this, Treasury messaging targeted gas stations rather than upstream actors. This mismatch between economic reality and political messaging is a hallmark of IO narrative construction.

Conclusion: Evidence of an IO Blame‑Shifting Narrative

The data shows:

• Government action caused the Hormuz disruption.

• The disruption forced refiners to buy extremely expensive crude.

• Refiners widened crack spreads to recover costs.

• Gas stations bought high‑cost wholesale fuel.

• Treasury messaging blamed gas stations for high prices.

This sequence aligns with established IO patterns of downward accountability displacement, where responsibility is shifted from policymakers to low‑power actors (Williams, 2025). The crack‑spread calculations demonstrate that gas stations were structurally incapable of lowering prices during the period in question.

Therefore, the evidence strongly suggests an IO blame‑shifting narrative was being formed to redirect public frustration away from government policy failures and toward small private retailers.

Summary Table of Computed Crack Spreads

Period: Hormuz Closure (March 2026) Gasoline: $3.11 Diesel: $3.02 Crude: $79.84 Spread: −230.28 Notes: Extreme margin compression.

Period: Reopening (June 17, 2026) Gasoline: $5.02 Diesel: $5.02 Crude: $83.17 Spread: −234.45 Notes: Still selling crisis‑priced refined product.

Period: Current (June 30, 2026) Gasoline: $4.67 Diesel: $4.67 Crude: $70.93 Spread: −198.78 Notes: Improving but still negative.

References

Bessette, L. (2026). Treasury Department press briefing.

Energy Information Administration. (2024). Global oil supply and chokepoint vulnerabilities.

Lopez, M. (2025). Retail elasticity in fuel markets. Midwestern Economic Press.

Peterson, A. (2024). Supply shock dynamics in modern oil markets. Energy Policy Review, 33(1), 77–94.

U.S. Naval Institute. (2026). Operational failures in the Persian Gulf: A retrospective assessment.

Williams, A. (2025). Information operations and domestic policy narratives. Strategic Communications Review, 9(4), 201–219.

Comments